Total M&A Value Down 68% In 2015

By Ben Rye, Sayer Energy Advisors

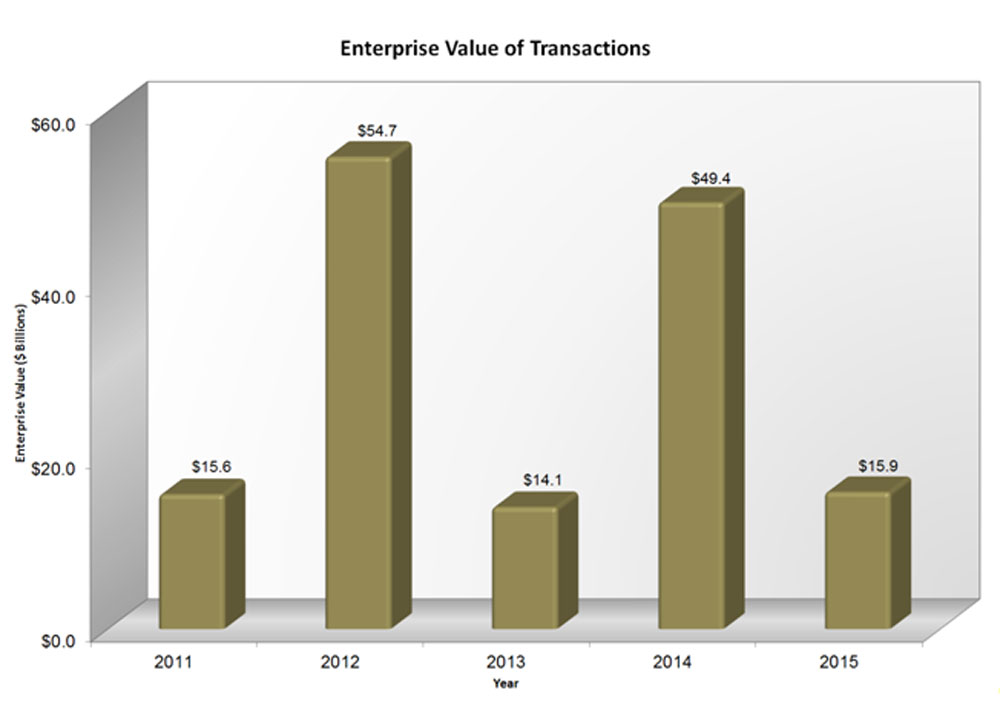

The total enterprise value of merger and acquisition (“M&A”) transactions in the Canadian oil and natural gas industry plummeted 68% in 2015, falling to $15.9 billion from the $49.4 billion recorded in 2014. In contrast, M&A activity in 2014 had surged 254% to $49.4 billion from the $14.1 billion of M&A activity recorded in 2013. The surge in M&A activity in 2014 was primarily driven by total financings of $24.0 billion, which was the second highest value in the last decade.

For a larger image click here !

{kind=link}

There were four deals valued at over $1 billion in 2015 compared to ten such deals in 2014 and two in 2013. The largest transaction in 2015 was Cenovus Energy Inc.’s sale of its royalty business, Heritage Royalty Limited Partnership, a wholly-owned subsidiary, to Ontario Teachers’ Pension Plan (“OTPP”) for gross cash proceeds of approximately $3.3 billion. The sale of Cenovus’s royalty business to OTPP was counted as a property deal, swinging the bulk of the total M&A value to property deals in 2015. The largest corporate transaction in 2015 was the purchase of Legacy Oil + Gas Inc. by Crescent Point Energy Corp. for approximately $1.8 billion.

A large transaction which contributed approximately 37% of the total enterprise value of M&A activity in the fourth quarter of 2015 was the acquisition of the majority of Canadian Natural Resources Limited’s royalty interests by PrairieSky Royalty Ltd. for $1.8 billion. The fourth billion dollar transaction is the pending acquisition of Long Run Exploration Ltd. by Sinoenergy Investment Corp. for approximately $1.1 billion.

There were 88 deals valued at over $5 million (large deals) in 2015, a decrease of 47% from the 165 large deals which took place in 2014. Of the large deals in 2015, the number of oil-weighted transactions was 55, a 38% drop from 88 in 2014. There were 33 large natural-gas weighted transactions in 2015 compared to 77 in 2014, a 57% decrease.

In comparing total M&A value on a commodity basis, natural gas-weighted deals plunged 87% to $5.1 billion in 2015 from $38.5 billion in 2014, accounting for substantially all of the decrease in activity level year-over-year. Oil-weighted deals dipped 6% to $9.9 billion from the $10.5 billion recorded in the previous year. Oil-weighted deals accounted for two thirds of the M&A value of large deals in 2014.

Of the $15.0 billion in total enterprise value of large deals in 2015 (over $5 million in size), there were 23 corporate transactions and 65 property deals. The value split between corporate and property deals in 2015 was $6.0 billion weighted toward corporate transactions and $9.0 billion in property deals. In 2014 there were 165 large deals, of which 30 were corporate transactions and 135 were property transactions. This is the third straight year in which the value of property transactions has been higher than corporate transactions.

One of the trends we saw progressing in 2015 was the growing number of transactions involving royalty interests. The largest royalty transaction was the previously mentioned sale of Cenovus’s royalty business to OTPP for $3.3 billion. PrairieSky was active in purchasing royalty interests as seen in its previously mentioned purchase of royalty assets from Canadian Natural Resources, as well as asset acquisitions from Manitok Energy Inc., Perpetual Energy Inc. and Traverse Energy Ltd.

Also in 2015, Freehold Royalties Ltd. purchased mineral title and royalty interests from Penn West Petroleum Ltd. for $318.0 million, as well as assets from Manitok. Finally, Maple Leaf Royalties Corp. acquired royalty and working interests from two Maple Leaf funds before being acquired corporately by Eagle Energy Trust.

Another trend we saw in 2015 was the emergence of hostile takeovers, which have not been very common in the Canadian marketplace. In 2015, Suncor Energy Inc. announced its intention to acquire all of the issued and outstanding shares of Canadian Oil Sands Limited (“COS”) for consideration of 0.25 of a Suncor share for each outstanding COS share. COS’ board of directors and major shareholders rejected the initial offer in hopes of the appearance of a “white knight.” On Jan. 18, 2016, Suncor increased its offer to 0.28 of a Suncor share for each outstanding COS. The amended offer, with a total aggregate transaction value of approximately $6.6 billion including COS estimated debt of $2.6 billion had the support of the board of directors of both companies.

Also in late 2015, 1927297 Alberta Ltd. announced its intention to acquire all the common shares of Ironhorse Oil & Gas Inc. for $0.17 per share. The shareholders of Ironhorse rejected the proposed transaction.

Since the beginning of 2016 we have seen a number of companies such as Advantage Oil & Gas Ltd., Raging River Exploration Inc., RMP Energy Inc., Seven Generations Energy Ltd., Spartan Energy Corp., Tamarack Valley Energy Ltd. and Tourmaline Oil Corp. raise equity which is a sign that investor interest is returning to the industry. If these financings continue we should expect to see a higher amount of M&A activity in 2016 than what we saw in 2015.

- Sections:

- M&A

- Categories:

- Analysis

- Corporate Mergers