Sponsored Content – Living In Challenging Times: Energy Market Update

Energy White Paper

By ATB Financial

Industry Overview

These are indeed challenging times, though anyone involved in the energy industry for more than a decade has encountered at least one downturn. The industry itself has changed significantly since 2014 and is facing unprecedented uncertainty. Throughout this article we examine some of the factors that make up this current down cycle, as well as some of the courses of action available for companies on both the producer and services side of the equation. While the challenges facing the industry are significant, there are still reasons to be optimistic.

Commodities Update

With the cyclical nature of the energy industry, downturns are nothing new. In fact, we’re experiencing our seventh down cycle since the 1980s. We’ve seen the price of West Texas Intermediate (WTI) drop from a high of $110.53 per bbl on September 6, 2014, to about $30 per bbl in January 2016.

While the crash in oil prices have grabbed all the media attention, natural gas prices have quietly fallen 50-60 per cent since October 2014, with futures prices recently hitting a 16-year low with AECO being C$0.87 per mcf as of March 31, 2016.

Canada’s gas production has remained relatively flat, while gas exports to the U.S. have decreased 30 per cent since 2007. Meanwhile, U.S. gas production has increased despite low prices. Rapid production growth in the Marcellus Basin in the Eastern U.S. has outpaced transportation capacity and a wave of new pipelines are being constructed to move this gas to markets in the Northeast U.S., Eastern Canada and the U.S. Midwest. Without additional diversification and export capacity, Canada’s gas industry will continue to experience negative pressure due to ongoing competition from U.S. shale production.

{kind=link}

For a larger image click here !

LNG will play a significant role in determining the future of Canada’s natural gas industry. However, there remains a large amount of uncertainty within the global LNG market — including the forecasted economic growth, proposed gas pipelines from Russia, and the future energy mix which includes Japanese nuclear power and restrictions on coal use, especially in China.

Many LNG project sponsors have opportunities around the world, and remain focused on allocating capital toward areas with the best returns. While Canada unquestionably has attractive LNG resources, we face a number of challenges including lack of infrastructure; labour; regulatory constraints; First Nations priorities; and environmental concerns.

In regards to oil prices and supply, there are a wide range of oil price forecasts, from $15 per bbl to $80+ per bbl over the next year. During a price war, producers initially tend to increase production to maintain revenue. Saudi Arabia and Russia (the world’s two largest oil producers) both increased production last year. U.S. production has proved to be resilient; however declines of 0.6-1.0 million bbls per day in 2016 are expected over the next 12 months. It needs to be clear however that there are large volumes of reserves waiting for a price response. As such, we can expect the price recovery to be somewhat “choppy” as the supply/demand imbalance gets sorted out.

While many market participants are focused on supply, increased demand is needed to balance the market. Decelerating Chinese growth rates have contributed to a bear market for most commodities, and all oil demand growth is forecast to come from non-OECD countries.

{kind=link}

For a larger image click here !

Large corporate investment decisions are generally not made on near-term price swings. Keeping the longer-term picture in perspective is important as the potential overcorrection of capital could have serious consequences. There does continue to be stable demand growth of 1-2 million bbls per day into the foreseeable future as current expected renewable growth rate will not meet future energy needs.

Economic Landscape

The cyclicality of the energy industry at a commodity level directly affects a number of factors that in turn affect energy companies and impact the speed of recovery for the economy as a whole. These industry pressures include: government policy changes; regulatory regime; equity and public debt markets; M&A activity; E&P leverage; industry consolidation; and capital structure.

The energy sector directly accounts for about 66 per cent of Alberta’s private non-housing capital spending, and contributes approximately 25 per cent of GDP. Entering the downturn, companies quickly cut capex to protect their balance sheets. Capital investment dropped some 42 per cent in 2015, approximately $35 billion. While upstream oil and gas is still the largest private sector investor in Canada, capex is expected to drop an additional 26 per cent or about $12 billion in 2016.

{kind=link}

For a larger image click here !

In terms of impact on employment, it is significant and real. We all know people who’ve been affected. Alberta’s unemployment rate is the highest in 20 years and the number of EI recipients has doubled year-over-year. CAPP estimates there were 40,000 direct layoffs and close to 100,000 direct and indirect jobs lost across Canada in 2015 — considerably more than the 15,000–20,000 direct drilling jobs estimated lost during the 2008-2009 downturn. In fact, current layoffs compare to the 1982–1990 (NEP & supply glut). Not everyone remembers these challenges.

Much of the employment in the oilsands was from construction of large-scale mining operations. With no new mines in the foreseeable future, oilsands labour demand is not expected to return to peak levels. The era of junior oilsands companies may be under significant contraction as it appears to be a marketplace reserved for the majors. The industry has experienced another round of layoffs and the expectation is for more layoffs to come along with consolidation, forcing some permanent workforce reductions.

Market Consolidation

This prolonged period of lower commodity prices has created challenges for companies with high leverage, decreasing cash flows and limited hedges in place. Reduced capital expenditures and further decreases to cash flows will force companies to adjust their business plans to protect the balance sheet; aggressively cutting dividends; reducing cost structures by 20-30 per cent through layoffs, reduced work weeks, and bonus and salary reductions; and increasing pressure on suppliers.

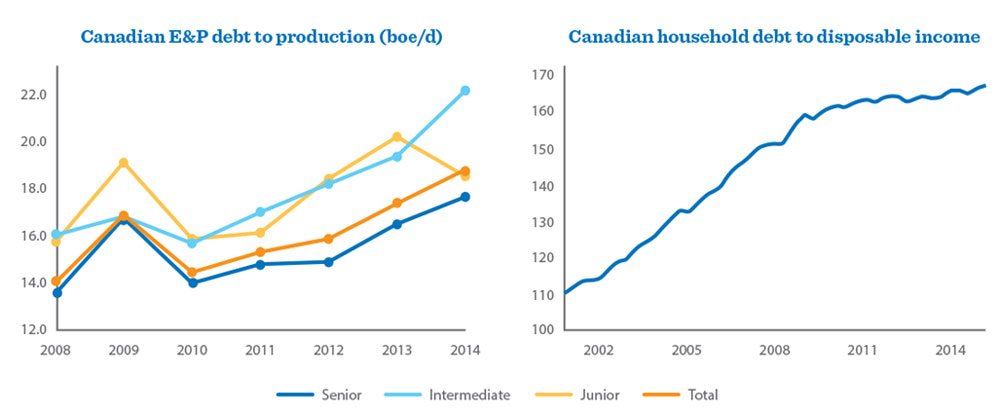

Companies with high leverage will struggle as traditional sources of alternative capital may not be readily available. Many will likely see a reduction to their credit facilities at next review, and lender patience extended last spring will get stretched as the downturn persists. Another challenge to be addressed is how to fund reserve growth as we move forward to offset the natural declines in production that occur in the basin.

{kind=link}

For a larger image click here !

E&P companies have already squeezed suppliers for cost savings of 20-30 per cent. This has eliminated profits for many service companies and some are performing unprofitable work just to maintain market share. For the energy sector to survive an extended downturn, Canada’s cost structure must be reduced to compete on a global basis, while still providing an appropriate return on invested capital.

The next major round of cost cutting can only be achieved through consolidation. Companies (and capital providers) can only wait out the downturn for so long. The oilfield services sector is overbuilt for current conditions and companies must materially reduce staff and G&A. Drilling activity in Q2/16 could be down over 40 per cent year-over-year, and some service companies may not survive through the summer.

Despite pressures for consolidation, M&A activity has remained slow. Bid-ask spreads persist due to commodity price fluctuations. In excess of $10 billion (CDN private equity, US private equity, Asian investors, and companies that already have capital in place) is available to deploy, but on what terms? We expect activity to pick up as companies are forced to begin marketing their quality assets and/or pursuing corporate sales.

{kind=link}

For a larger image click here !

Sources of Capital

Investors have many opportunities globally and attracting efficient capital is critical in developing Canada’s energy industry. In the 1990s, Canada attracted 37 per cent of North American oil and gas investments; however this is down to 17 per cent today. More Canadian projects have been cancelled or scaled back than anywhere else in the world. Even prior to the downturn we were in the midst of an investor shift away from mega-projects with long payback periods and higher associated risk/uncertainty, moving toward smaller projects with quicker payout periods and less perceived risk.

Bank debt has traditionally been a key source of capital for junior and intermediate companies, with the size of E&P credit facilities primarily driven by the quantity of reserves and commodity price forecast. On average, we have seen an approximate 40 per cent reduction in E&P lending value year-over-year as of October 1, 2015. Some institutions are aggressively cutting exposure to the energy sector as losses are being realized.

Over the past 12–18 months we have also seen fewer equity financings. Select senior and intermediate companies were responsible for the majority of the new equity issuances in 2015, with limited equity raised in the past six months. Corporate sales/consolidations are likely the best solution for the junior market and select intermediates that missed the limited and highly selective equity window.

Looking Forward

The challenges facing the energy industry are real, significant and unprecedented. Prices will likely be “lower for longer,” looking well into 2016 or even 2017 for any meaningful price recovery. And, there is likely more pain to come in 2016 with further cuts to capital spending and additional layoffs.

Although commodity prices are cyclical, we are unlikely to return to “business as usual.” Prior to the downturn, the industry was experiencing transformational shifts not seen in 100 years. Examples include an investor shift away from mega-projects, advancements in drilling and completions technology, global pressure on carbon emitters, and the fact that U.S. shale has turned oil into a “just in time” delivery product.

Consolidation will likely become a key theme across the industry as companies take steps to protect their business and shareholders. Companies may be evaluating their interim financing options, including restructuring credit facilities, removing non-consenting lenders and looking to potential equity partners.

Despite industry challenges, there are still reasons to be somewhat optimistic. The downturn may drive long overdue cost reductions and much-needed consolidation, resulting in a stronger and more efficient industry down the road. This may provide an attractive upside for potential investors with a longer-term investment horizon. Also, we are witnessing technological advancements that are real, significant and true game changers for the industry. Alternative and renewable energy advancements are also on the forefront, although scalability advancements are still in development.

From a banking standpoint, at ATB, we strive to find ways to continue to support our customers despite the stressed environment. We are here for the genuine pursuit of Alberta’s greater good. We know that our clients and all of Alberta is full of great and innovative leaders that have made this province great. By listening to Albertans, and to our clients, we look to support this innovation and leadership and truly make banking work for people.

- Categories:

- Sponsored Content